CIRI mailed IRS 1099 forms to all shareholders for the 2014 tax year on January 29, 2015. You may receive more than one type of Form 1099, depending on the type of income received from CIRI. The 1099 forms reflect payments including:

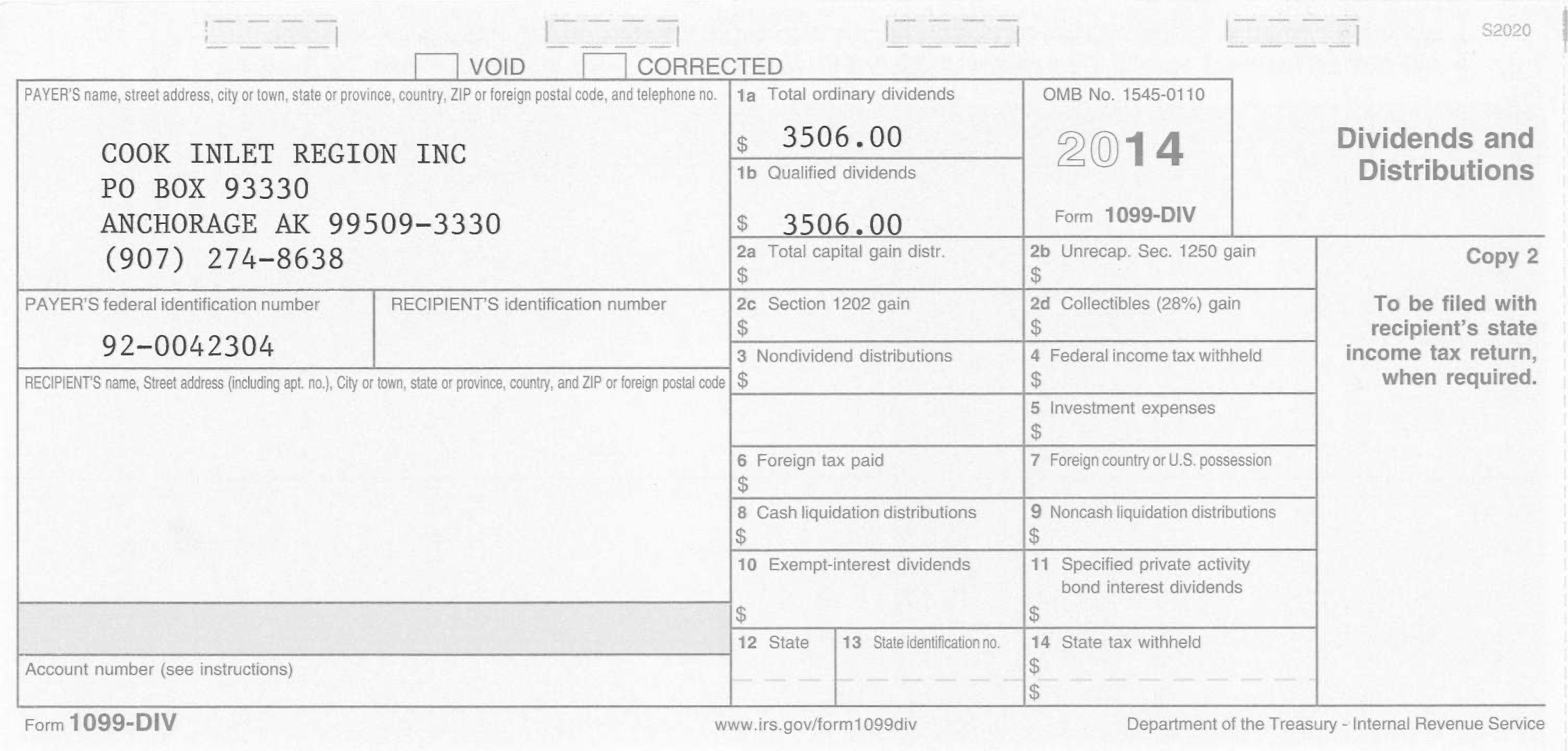

- Quarterly dividends (reported in boxes 1a and 1b on Form 1099-DIV)

- CIRI Elders’ Settlement Trust distributions (reported in boxes 1a, 1b and 3 on Form 1099-DIV)

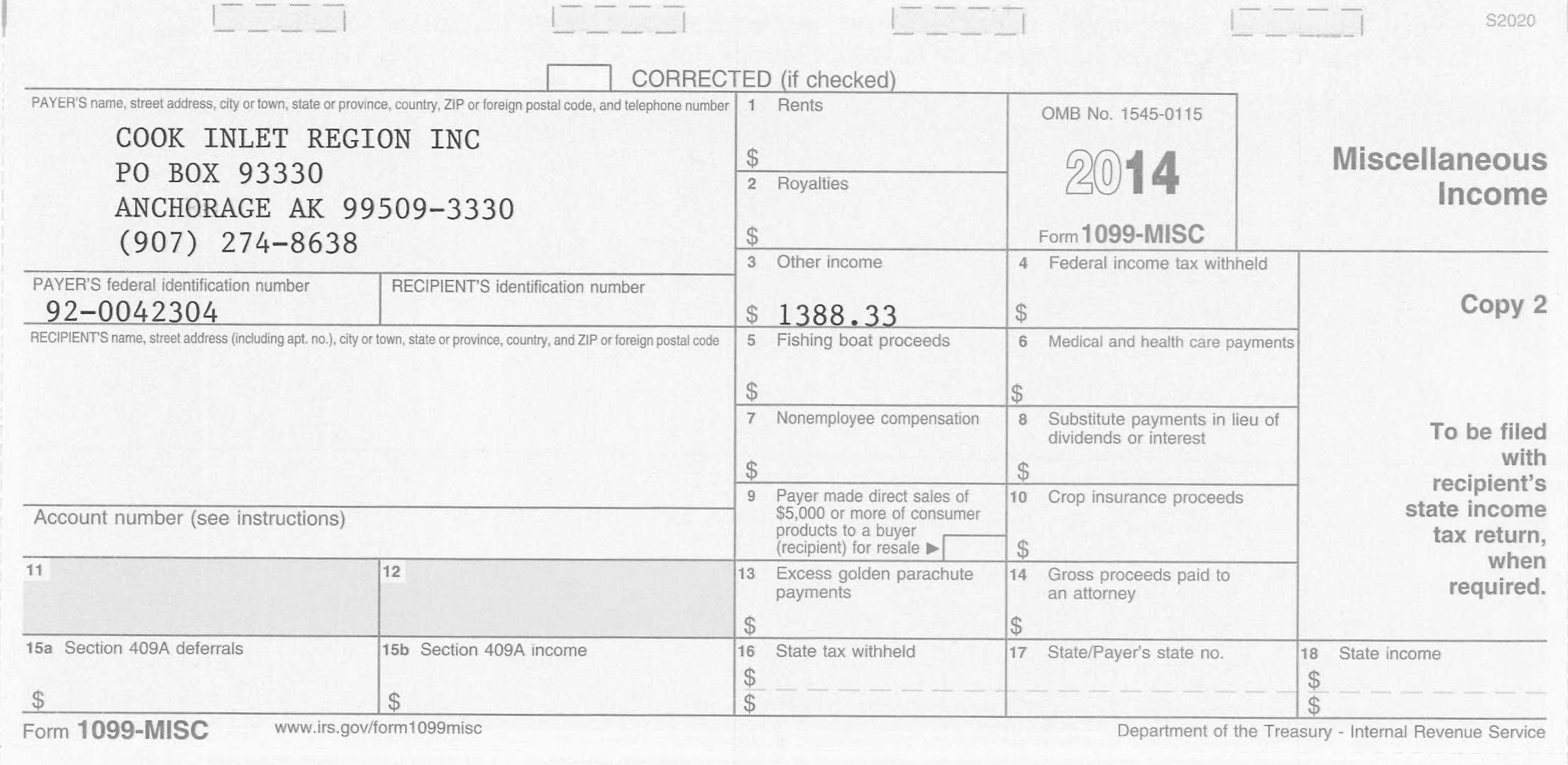

- 7(j) resource payments (reported in box 3 on Form 1099-MISC)

- Shareholder prizes (reported in box 3 on Form 1099-MISC)

CIRI paid $35.06 per share (or $3,506 per 100 shares) in quarterly dividends in 2014, which were reported on a 1099-DIV in both Box 1a – Ordinary Dividends, and Box 1b – Qualified Dividends. The Box 1a amount is the total of all taxable distributions CIRI paid for dividends and Elders’ Benefit Program distributions. Box 1b shows the same amount and may qualify for a reduced tax rate. If you have held your shares for less than one year, please consult your tax advisor regarding the proper treatment of qualified dividends.

If you inherited new shares during 2014 you may have an amount reported in box 3 (nondividend distributions) on the 2014 Form 1099-DIV. Please consult your tax advisor for the appropriate treatment of distribution totals reported in box 3. In some circumstances, depending upon an individual’s tax “basis” in their stock, some or all of the box 3 total could be subject to tax.

Distributions received in 2014 from the Elders’ Benefit Program are also reported by CIRI on a Form 1099- DIV, both in box 1a (ordinary dividends) and in box 1b (qualified dividends). However, CIRI Elders’ Settlement Trust payments had both a taxable and nontaxable portion, with the taxable portion reported in Boxes 1a and 1b on a 1099-DIV, and the nontaxable portion reported in Box 3 (nondividend distributions). If you received all four Elders’ Trust payments last year, $1,382.74 is reported in Boxes 1a and 1b, and the remaining $417.26 is reported in Box 3.

At-large shareholders received a $13.8833 per share (or $1,388.33 per 100 shares) 7(j) resource revenue payment in 2014. If you are an at-large shareholder, your 7(j) payment is reported on a Form 1099-MISC in box 3 (other income). The resource revenue payment derives from resource sharing among the 12 regional corporations as required by the Alaska Native Claims Settlement Act. Your 7(j) payment appears on a different form because resource revenue payments are not dividends and are not considered investment income. ANCSA requires that resource revenue be paid to village shareholders’ village corporations, so that CIRI does not report these payments as individual shareholder income. CIRI reports payments made in 2014 to shareholders for prizes or awards on Form 1099-MISC in box 3 (other income).

The proper IRS forms and schedules to use when completing your tax return may vary depending on the types of CIRI payments received. For example, IRS instructions stipulate that IRS Form 1040A is not the proper form to use if a 1099-MISC was received. Remember, it is your responsibility to accurately report your CIRI income on your tax returns. While we hope this information has been helpful, it does not constitute tax advice, particularly as it relates to any individual reporting situation. CIRI cannot provide tax advice. Shareholders are encouraged to consult with a tax advisor regarding individual circumstances and applicable federal and state tax requirements.