Important Dates

Elders’ Settlement Trust payments

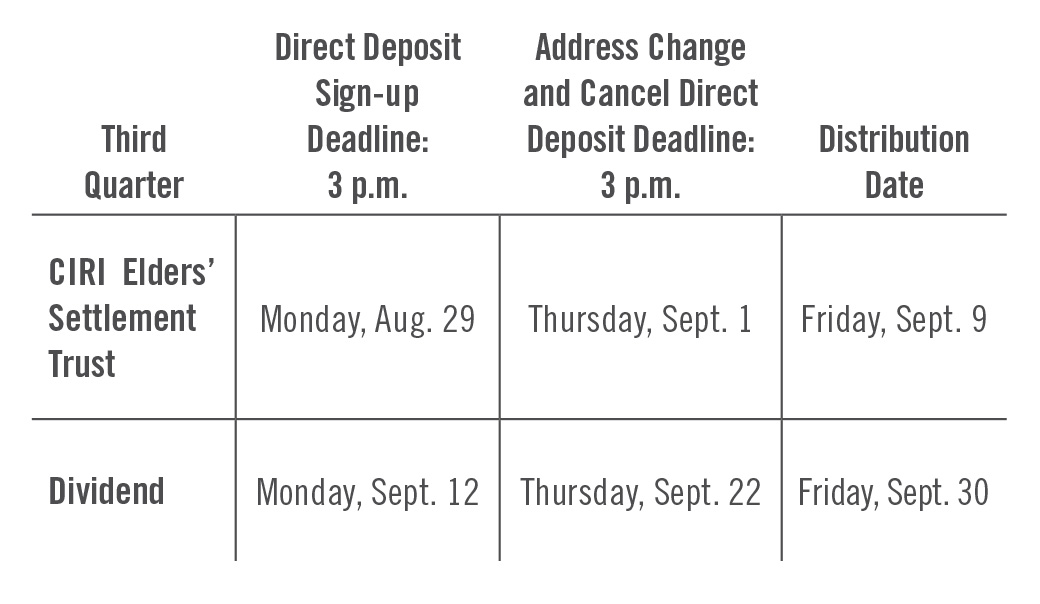

The third quarter CIRI Elders’ Settlement Trust payment of $450 is scheduled for Friday, Sept. 9, with the final 2016 Elders’ payment scheduled for Friday, Dec. 9. Original shareholders who are 65 years of age or older and who own at least one share of CIRI stock as of the distribution dates are eligible to receive the Elders’ Trust payments. For the September distribution, eligible Elders who have their CIRI dividends directly deposited will have their trust payments electronically transmitted by 6 p.m. Alaska Daylight Time on Friday, Sept. 9, with checks mailed to the remaining eligible Elders that same day.

CIRI shareholders voted in June 2003 to establish the Irrevocable Elders’ Settlement Trust. In accordance with the vote, CIRI initially funded the Trust with a $16 million contribution. At the time, it was anticipated that Elders would receive quarterly distributions of $450 until 2023. This projection was based upon assumptions regarding the performance of Trust investments over time and the number of beneficiaries.

However, as discussed in the survey results mailed to shareholders in early 2015, due to the 2008 global economic downturn on investments and the fact that shareholders are living longer than anticipated, the Trust could run out of money as early as 2019. The Trustees are working with CIRI to explore potential options for additional funding to extend the life of the Trust. Any news regarding the future of the Elders’ Settlement Trust will be shared in the Raven’s Circle and by other means.

Third Quarter Dividend

On Friday, Sept. 30, CIRI will mail or directly deposit third quarter 2016 dividends in the amount of $8.70 per share (or $870 if you own 100 shares of stock) to all shareholders with a valid mailing address on file as of 3 p.m. Thursday, Sept. 22. If you participate in direct deposit, your dividend will be electronically transmitted to your account by 6 p.m. Alaska Daylight Time on Sept. 30.

Direct Deposit

Shareholders who participate in direct deposit and have a current CIRI mailing address are eligible to participate in quarterly prize drawings. Direct deposit forms are available from Shareholder Relations and at ciri.com. To cancel direct deposit, please submit a signed, written request prior to 3 p.m. on the specified deadline.

Address Changes

Checks and vouchers will be mailed to the address CIRI has on record as of the specified deadline. If your address has changed, be sure to update your address with both CIRI and the U.S. Postal Service. These addresses must match or your CIRI mail may not reach you. When CIRI mail is returned as undeliverable, distributions are held and the shareholder does not qualify to participate in any prize drawings until the address is updated. This is true even if a shareholder has his or her dividends electronically deposited.

CIRI address change forms can be downloaded and printed at ciri.com, or you may send a signed, written address change request that includes a current telephone number. Address change forms can be mailed to CIRI at PO Box 93330, Anchorage, AK 99509, scanned and emailed to shareholderrecords@ciri.com or faxed to 907-263-5186. If faxed, please call Shareholder Relations as soon as possible to confirm receipt. Forms and information on changing your address or submitting a mail-forwarding request with the U.S. Postal Service are available at www.usps.com or at your local post office.

Please be aware that if you fail to notify CIRI of your new address before the deadline, and your check is sent to your old address, CIRI cannot reissue that check to you unless it is either returned to Shareholder Relations or a minimum of 90 days has elapsed.

Tax Reminder

As a reminder, CIRI does not withhold taxes from distributions; however, shareholders who anticipate owing tax on their distributions have the option of making quarterly estimated tax payments directly to the IRS. To find out more about applicable federal and state tax requirements or making quarterly estimated tax payments, please consult with a tax advisor or contact the IRS directly